UN RECOUVREMENT DE L’IMPÔT FONCIER LIMITE PAR SON MODE DE GOUVERNANCE EN CÔTE D’IVOIRE : CAS DE VILLE DE BOUAKE

RESUME :

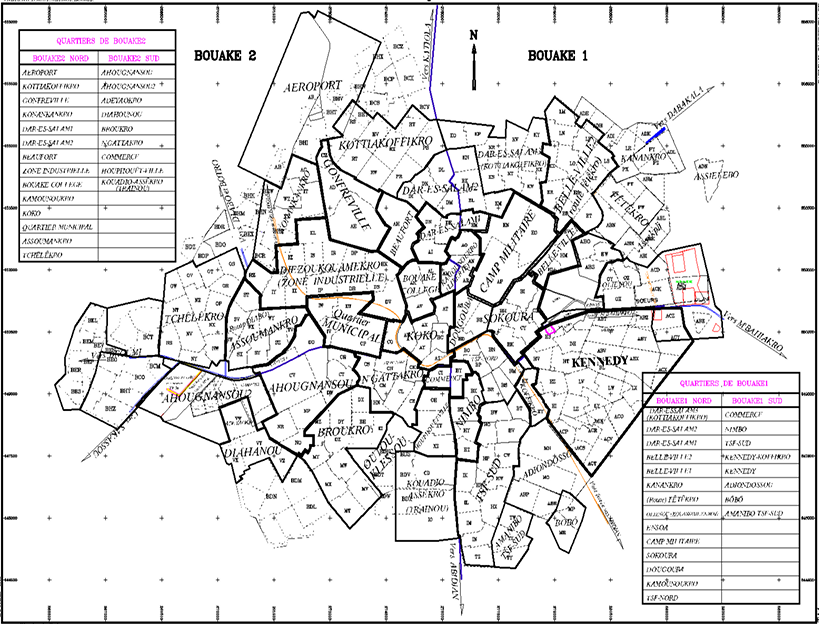

Le système fiscal ivoirien prévoie le paiement de l’impôt foncier sur les propriétés bâtis ou non. Contrairement à la métropole abidjanaise où la collecte de cet impôt est rigoureusement organisée et suivie par les services des impôts, les villes de l’intérieur du pays comme Bouaké, connaissent des recouvrements de l’impôt foncier relativement faibles au regard du volume de leur assiette fiscale foncière. Le système en vigueur prévoit l’octroi intensif d’exonérations et de mesures dérogatoires pour booster le paiement de l’impôt. Cependant, il y a une sous-mobilisation de cette recette fiscale. Cette recherche est donc une analyse de la gouvernance du recouvrement de l’impôt foncier sur l’espace urbain de Bouaké. Parti d’une recherche documentaire, l’étude est conduite à partir d’entretiens réalisés auprès des autorités déconcentrées de l’administration fiscale et de la marie, et d’un questionnaire administré aux chefs de ménage. Au terme des investigations, il ressort que les populations ont une vague perception de l’impôt foncier et de son utilité dans un conteste national où son paiement est fait sur une base déclarative. De plus la faible implication des autorités décentralisées dans le recouvrement de l’impôt foncier et l’imparfaite conception de la matrice cadastrale constituent des facteurs limitants. Une réforme de la législation fiscale qui donne des prérogatives en matière de perception de l’impôt foncier aux collectivités territoriales s’avère nécessaire.

Mots clés :Côte d’Ivoire, Bouaké, Gouvernance, impôt foncier

ABSTRACT

PROPERTY TAX COLLECTION LIMITED BY ITS GOVERNANCE MODEL IN CÔTE D’IVOIRE: THE CASE OF THE CITY OF BOUAKE

The Ivorian tax system provides for the payment of property tax on both built and unbuilt properties. Unlike in the city of Abidjan, where the collection of this tax is rigorously organised and monitored by the tax authorities, towns in the interior of the country, such as Bouaké, have relatively low property tax collection rates in relation to the size of their property tax base. The current system provides for the intensive granting of exemptions and derogations to boost tax payments. However, there is under-mobilisation of this tax revenue. This research is therefore an analysis of the governance of property tax collection in the urban area of Bouaké. Based on documentary research, the study is conducted through interviews with decentralised tax administration and municipal authorities, and a questionnaire administered to heads of households.At the end of the investigations, it appears that the population has a vague perception of property tax and its usefulness in a national context where payment is made on a declarative basis. Furthermore, the limited involvement of decentralised authorities in property tax collection and the imperfect design of the cadastral matrix are limiting factors. A reform of tax legislation that gives local authorities powers to collect property tax is necessary.

Key words: Côte d’Ivoire, Bouaké, Governance, property tax